How Artificial Intelligence Is Disrupting Finance

As consumers, we’re familiar with AI: we benefit from cars that parallel park themselves, devices that respond when asked questions, and streaming platforms that suggest shows we may like. However, professionally, the larger question is how industries will harness the power of AI. In finance, AI offers opportunities for operational efficiencies in everything from risk management and trading to insurance underwriting.

As consumers, we’re familiar with AI: we benefit from cars that parallel park themselves, devices that respond when asked questions, and streaming platforms that suggest shows we may like. However, professionally, the larger question is how industries will harness the power of AI. In finance, AI offers opportunities for operational efficiencies in everything from risk management and trading to insurance underwriting.

Melissa Lin

Melissa has worked in ECM, tech startups, and management consulting, advising Fortune 500 companies across multiple sectors.

Expertise

Executive Summary

Artificial Intelligence (AI) Is Exploding

- The widespread adoption of AI across industries is predicted to drive global revenues of $12.5 billion in 2017 and $47 billion in 2020 with a CAGR of 55.1% from 2016 to 2020, according to a 2016 report by IDC.

- The industries that will invest the most in these technologies are banking and retail, followed by healthcare and manufacturing.

- Economists designate general purpose technologies (GPT) as those important enough to spur protracted economic growth and societal advancements. For example, electricity is a GPT. A recent Harvard Business Review article designates AI as the most important GPT of our era.

Artificial Intelligence in Financial Services: Risk Management

- PayPal has been able to boost security by leveraging deep learning technology. PayPal's fraud is relatively low at 0.32% of revenue, a figure far better than the 1.32% average that merchants see.

- While a linear model can consume 20-30 variables, deep-learning technology can command thousands of data points.

Artificial Intelligence in Financial Services: AI Trading

- For years, investment management companies have relied on computers to make trades. Around 9% of all funds, managing $197 billion, rely on large statistical models built by data scientists.

- However, these models are often static, require human intervention, and don't perform as well when the market changes. Therefore, funds are increasingly migrating towards true artificial intelligence models that analyze large volumes of data and continue to improve themselves.

- In 2000, Goldman Sachs' US cash equities trading desk in its New York headquarters employed 600 traders. Today, it has two equity traders, with machines doing the rest.

Artificial Intelligence in Financial Services: Robo-Advisory

- For investors, robo-advice can offer up to 70% in cost savings in certain services.

- Some established investment firms are buying existing robo-advisors, such as Invesco's acquisition of Jemstep and Blackrock's purchase of FutureAdvisor. Others are even creating their own robo-advisors, such as FidelityGo and Schwab's Intelligent Advisory.

- 77% of wealth management clients trust their financial advisors and 81% indicate that face-to-face interaction is important.

Artificial Intelligence in Financial Services: Underwriting & Claims for Insurance

- A PWC report predicts that AI will have automated a considerable amount of underwriting by 2020, especially in mature markets where data is available.

- In a 2013 Oxford study analyzing over 700 professions to determine which were most susceptible to computerization, insurance underwriters were included in the top five most susceptible.

- Underwriting may leverage not only machine learning but also wearable technology and deep learning facial analysis technology.

Artificial Intelligence in Financial Services: Customer Service via Chatbots

- In October 2016, both Bank of America and MasterCard unveiled their chatbots, Erica and Kai, respectively. The early version of Erica can track customers' credit scores, look at their spending habits, and offer advice on how to pay off bills.

- Capital One also recently launched their own chatbot, named "Eno,"" which enables customers to chat with the bank using text-based language to pay bills and retrieve account information. Capital One also leveraged the internet-of-things trend, launching an Alexa Skill for Amazon Echo, and plans to be the first to launch a similar service for Microsoft’s Cortana.

General purpose technology is a term economists reserve for technologies that spur protracted economic growth and societal advancements, revolutionizing the operations of households and corporations alike. A sample general purpose technology is electricity. Electricity spawned a multitude of products and sectors, including refrigerators, washing machines, trains and, of course, computers. The advent of electricity radically transformed the world.

A recent Harvard Business Review article designates artificial intelligence (AI) as the most important general purpose technology of our era. We’re familiar with the power of AI. It manifests in the form of a robot defeating a world-renowned chess player. A car that can parallel park itself. Devices that respond with tomorrow’s weather when we ask. But much of our contact with—and understanding of—AI revolves around products that affect our everyday lives as consumers. At the organizational level, there’s a larger question around how AI will disrupt industries, and specifically, how financial services will harness AI.

The following article will define artificial intelligence, the sphere of its related technologies, the size of the overall AI industry, and the applications of artificial intelligence in finance. This piece is not intended to provide a normative judgment on AI development; rather, it will focus on how AI is disrupting finance.

Artificial Intelligence: What Is AI?

Artificial intelligence is an area of computer science focused on creating intelligent machines that function like humans. AI computers are designed to perform human functions including learning, decision making, planning, and speech recognition.

Artificial intelligence enables machines to continually improve their performance without humans providing prescriptive instructions for how to do so. This is significant for a couple reasons. First, humans know more than we are capable of telling. That is, humans may be able to recognize a face or execute a smart strategy in a game of chess. However, prior to advanced artificial intelligence technology, humans’ inabilities to articulate our knowledge meant that we couldn’t automate many tasks. Second, AI technology is superhuman in execution, operating more quickly and often with more accuracy than humans.

Artificial Intelligence Technologies

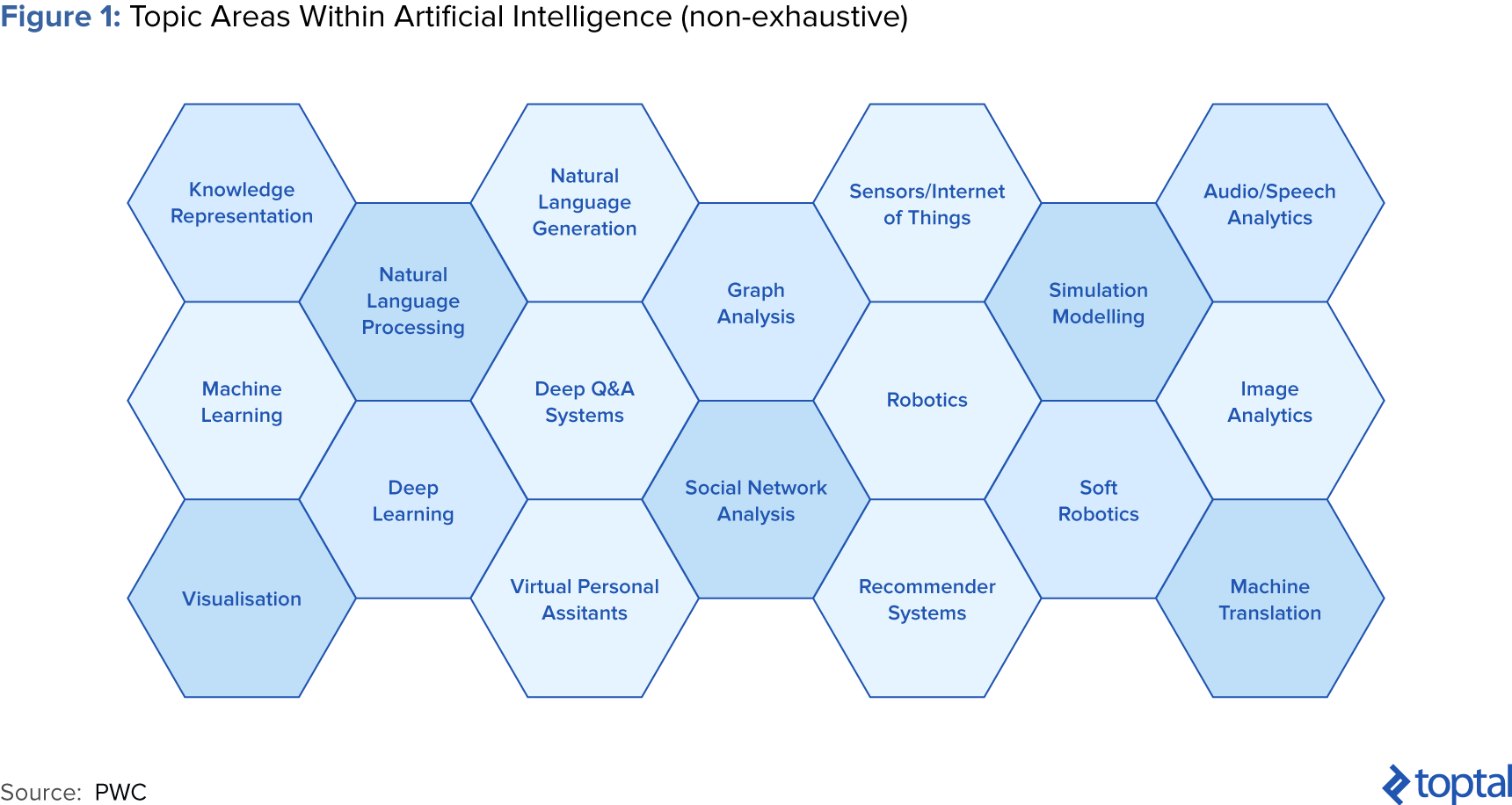

Artificial intelligence encompasses a multitude of capabilities and technologies. Consulting firm PWC reinforces that AI is “not a monolithic subject area. It comprises a number of things that all add to our notion of what it means to be ‘intelligent.’” Below are a few of the most popular areas of AI:

- Machine learning is a method of data analysis that automates analytical model building. Using algorithms that iteratively learn from data, [machine learning](https://www.toptal.com/machine-learning/machine-learning-theory-an-introductory-primer) enables computers to find hidden insights without being explicitly programmed where to look.

- Deep learning is a subset of machine learning. It has facilitated object recognition in images, video labeling, and activity recognition, and is making progress in perception (including audio and speech). For example, Facebook's deep learning application DeepFace has been trained to recognize people in photos. Many draw the comparison between deep learning technology and biology, but experts generally agree that while inspired by the human brain, it's not necessarily modeled after it.

- Natural language processing is the ability of a computer program to understand human speech in real time. Research and development is shifting towards systems capable of interacting with people through dialog, not just reacting to stylized requests.

- Internet of things (IoT) is devoted to the idea that a wide array of devices, including appliances, vehicles, and buildings can be interconnected. For example, if your alarm rings at 7:00 a.m., it could automatically notify your coffee maker to start brewing coffee for you. Wearable technologies that act as sensors when worn are also part of this larger trend.

Of course, this list is not comprehensive. See below for a wider range of artificial intelligence topics and technologies.

Artificial Intelligence Market Size

The aforementioned Harvard Business Review article predicts that “The effects of AI will be magnified in the coming decade, as manufacturing, retailing, transportation, finance, health care, law, advertising, insurance, entertainment, education, and virtually every other industry transform their core processes and business models to take advantage of machine learning. The bottleneck is in management, implementation, and business imagination.”

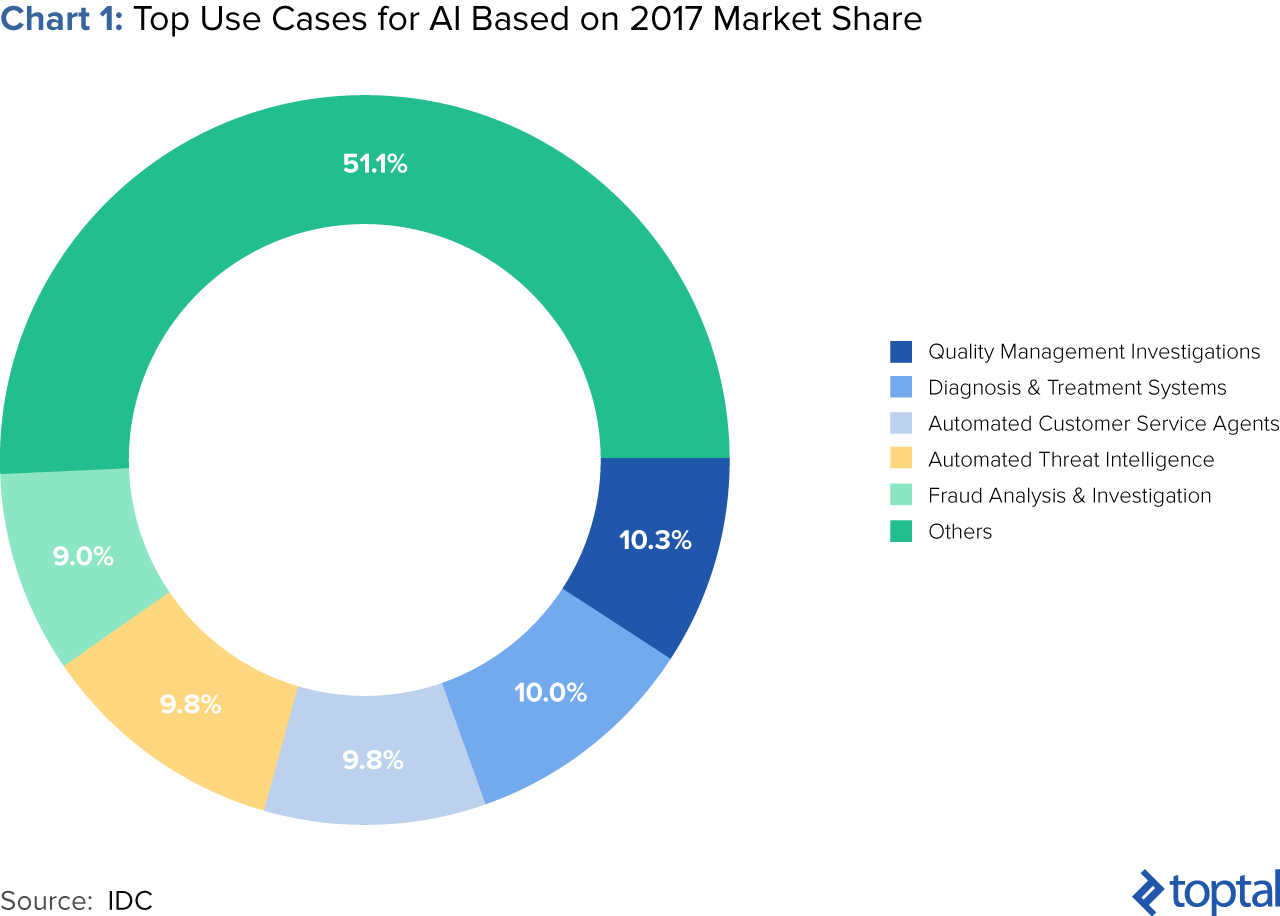

The widespread adoption of AI across industries is predicted to drive global revenues of $12.5 billion in 2017 and $47 billion in 2020 with a compound annual growth rate (CAGR) of 55.1% from 2016 to 2020. Specifically, the industries that will invest the most in the technology are banking and retail, followed by healthcare and manufacturing. In aggregate, these four industries will comprise over half of global AI revenues in 2016, with the banking and retail sectors each delivering nearly $1.5 billion.

Across industries, the greatest AI investments in 2017 will be in areas such as automated customer service agents, automated threat intelligence, and fraud analysis (see chart below). According to Jessica Goepfert, program director at market research firm IDC, “Near-term opportunities for cognitive systems are in industries such as banking, securities and investments, and manufacturing. In these segments, we find a wealth of unstructured data, a desire to harness insights from this information, and an openness to innovative technologies.” The next section of this article will delve into the various use cases for artificial intelligence in the financial services industry.

Present and Future Applications of Artificial Intelligence in Finance

Artificial intelligence in finance could drive operational efficiencies in areas ranging from risk management and trading to underwriting and claims. While some applications are more relevant to specific sectors within financial services, others can be leveraged across the board.

Artificial Intelligence in Finance: Risk Management

Artificial intelligence has proven extremely valuable when it comes to security and fraud detection. Traditional methods of fraud detection include computers analyzing structured data against a set of rules. For example, a given payments company might set a threshold for wire transfers at $15,000 so that any transaction exceeding that amount would be flagged for further investigation. However, this type of analysis produces many false positives and requires a lot of additional effort. Perhaps even more significantly, cybercrime fraudsters frequently change their tactics. Therefore, the most effective systems must continually become smarter.

With advanced learning algorithms, such as those from deep learning, new features can be added to the system for dynamic adjustment. According to Samir Hans, an advisory principal at Deloitte Transactions and Business Analytics LLP, “With cognitive analytics, fraud detection models can become more robust and accurate. If a cognitive system kicks out something that it determines as potential fraud and a human determines it’s not fraud because of X, Y, and Z, the computer learns from those human insights, and next time it won’t send a similar detection your way. The computer is getting smarter and smarter.”

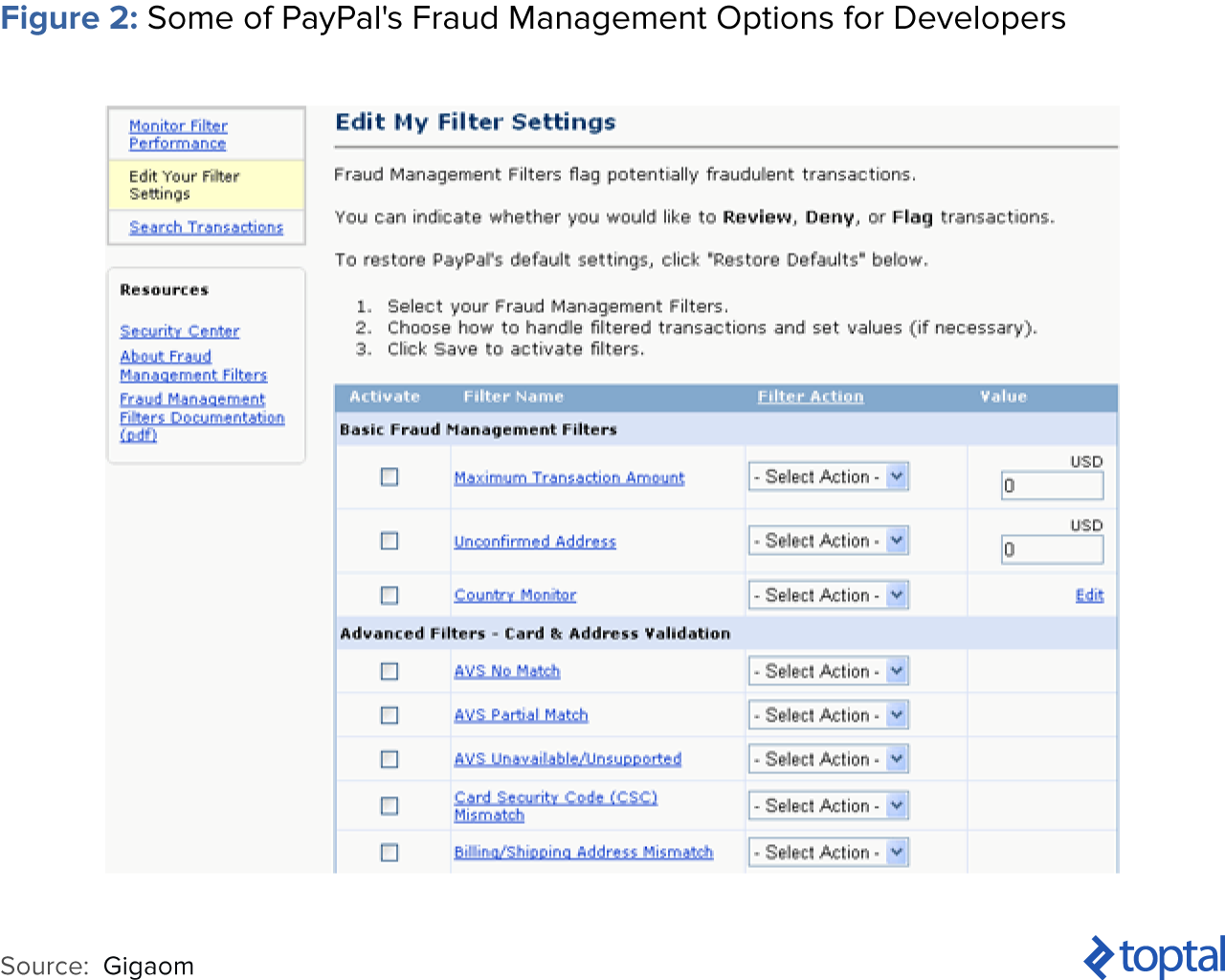

PayPal’s Success with Artificial Intelligence and Fraud Detection

Take payment giant PayPal and its advanced fraud protocols, for example. Due to its scale and visibility, PayPal “has a huge target on its back.” It processed $235 billion in 2015 from four million transactions by its 170 million customers. However, PayPal has been able to boost security by leveraging deep learning technology. In fact, PayPal’s fraud is relatively low at 0.32% of revenue, a figure far better than the 1.32% average that merchants see.

In the past, PayPal used simple, linear models. Today, its algorithms mine data from a customer’s purchase history and reviews patterns of likely fraud stored in its growing databases. While a linear model can consume 20-30 variables, deep-learning technology can command thousands of data points. These enhanced capabilities help PayPal distinguish innocent transactions from suspect ones. According to Hui Wang, PayPal’s Senior Director of Global Risk Sciences, “What we enjoy from more modern, advanced machine learning is its ability to consume a lot more data, handle layers and layers of abstraction and be able to ‘see’ things […] even human beings might not be able to see.”

Artificial Intelligence in Finance: Trading

Transition from Human-Constructed Models to True AI

For years, investment management companies have relied on computers to make trades. Around 1,360 hedge funds, representing 9% of all funds, rely on large statistical models built by data scientists often holding mathematics PhDs (otherwise known as “quants”). However, these models only utilize historical data, are often static, require human intervention, and don’t perform as well when the market changes. Consequently, funds are increasingly migrating towards true artificial intelligence models that can not only analyze large volumes of data, but also continue to improve themselves.

These new technologies utilize complex techniques including deep learning, a form of machine learning called Bayesian networks, and evolutionary computation, which is inspired by genetics. AI trading software can absorb enormous volumes of data to learn about the world and make predictions about the financial market. To understand global trends, they can consume everything from books, tweets, news reports, financial data, earnings numbers, and international monetary policy to Saturday Night Live sketches.

To be clear, the above is distinct from high-frequency trading (HFT), which allows traders to execute millions of orders and scan multiple markets in a matter of seconds, responding to opportunities in ways humans simply cannot. The AI-driven platforms discussed above are seeking the best trades in the longer-term, and machines—not humans—are dictating the strategy.

Some of these AI trading systems are developed by startups. For example, Hong Kong-based Aidiya is a fully autonomous hedge fund that makes all of its stock trades using artificial intelligence (AI). “If we all die,” says co-founder Ben Goertzel, “it would keep trading.” Traditional institutions are also interested in AI trading technology. In 2014, Goldman Sachs led the Series A funding round of and began installing an AI trading platform called Kensho. For Kensho’s Series B round, in addition to S&P Global, Wall Street’s biggest six banks (Goldman Sachs, JPMorgan Chase, Bank of America Merrill Lynch, Morgan Stanley, Citigroup, and Wells Fargo) also participated.

Trading Performance Comparison

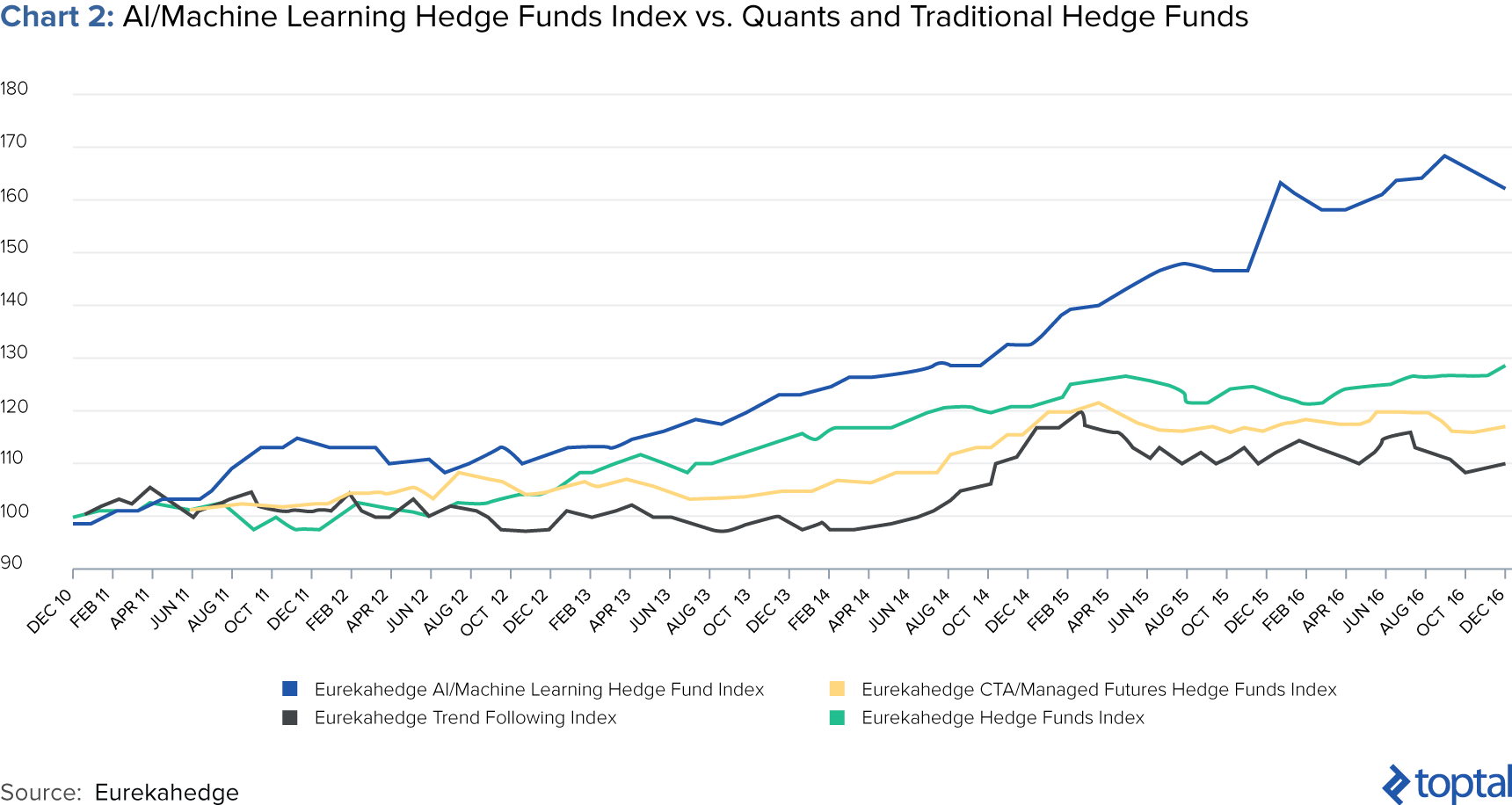

A recent study performed by investment research firm Eurekahedge tracked the performance of 23 hedge funds utilizing AI from 2010-2016, finding that they outperformed those managed by more traditional quants and generalized hedge funds.

Implications for Traders and Quants

It will be interesting to observe how AI will impact the trading labor market. Its effects are already apparent at some major banking institutions. In 2000, Goldman Sach’s U.S. cash equities trading desk in its New York headquarters employed 600 traders buying and selling stock. Today, it has two equity traders, with machines doing the rest. Daniel Nadler, CEO of Kensho, declares, “In 10 years, Goldman Sachs will be significantly smaller by headcount than it is today.” And as for the quants, they may find that their skills are in less demand from investment management companies.

Currently, about a third of graduates from top business programs feed into finance. Where would some of the nation’s best talent move to? Mark Minevich, senior adviser to the U.S. Council on Competitiveness, believes that “Some of these smart people will move into tech startups, or will help develop more AI platforms, or autonomous cars, or energy technology […] New York might compete with Silicon Valley in tech.”

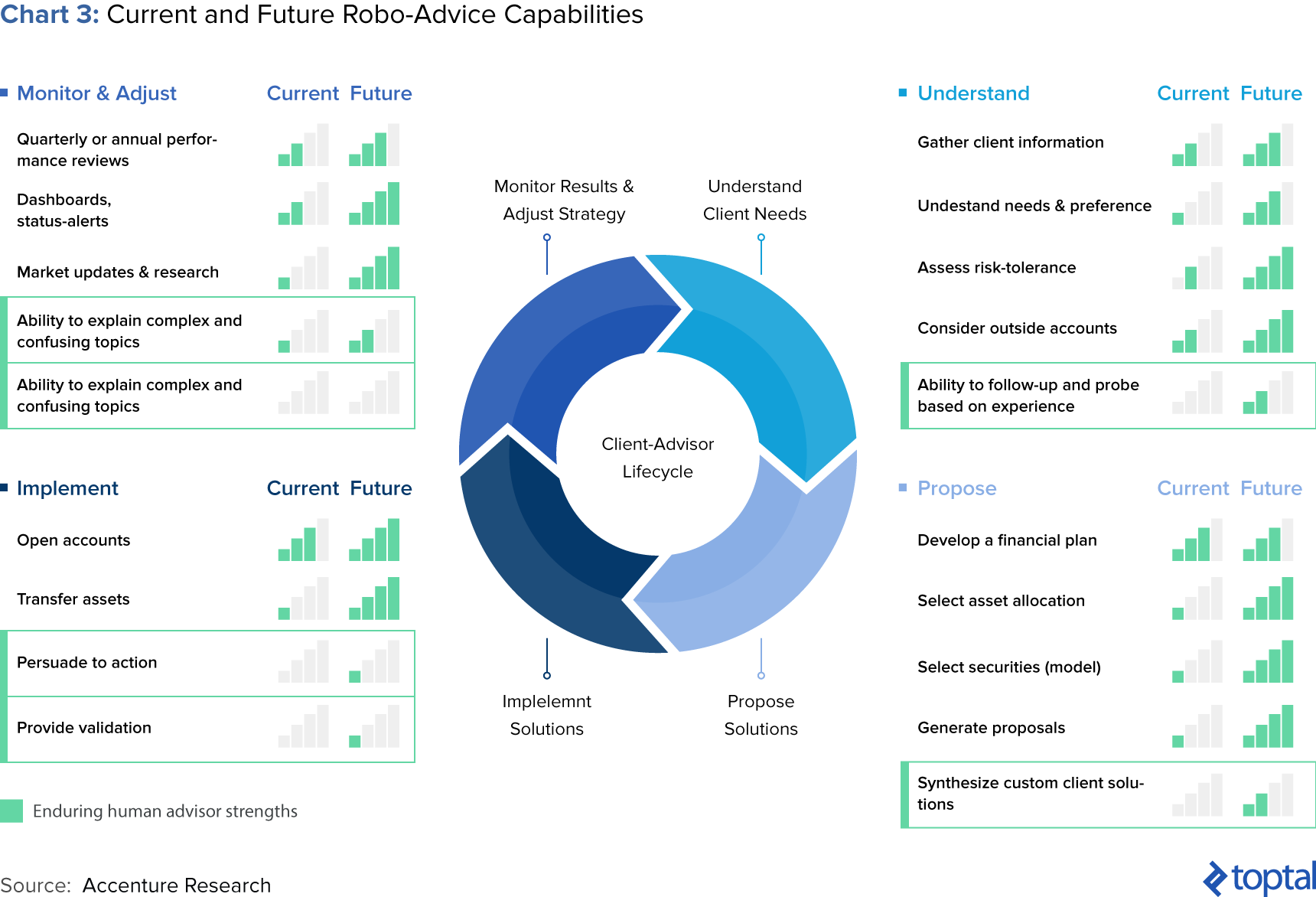

Artificial Intelligence in Finance: Robo-Advisory

What Is a Robo-Advisor and How Does It Work?

Robo-advisors are digital platforms that provide automated, algorithm-driven financial planning services with minimal human supervision. While human financial managers have been utilizing automated portfolio allocation since the early 2000s, investors had to employ advisors to benefit from the technology. Today, robo-advisors allow customers direct access to the service. Unlike their human counterparts, robo-advisors monitor the markets non-stop and are available 24/7. Robo-advisors can also offer investors up to 70% in cost savings and typically require lower or no minimums to participate.

Today, robo-advisors can help with the more repetitive tasks such as account opening and asset transferring. The process typically involves clients answering simple questionnaires about risk appetite or liquidity factors, which robo-advisors then translate into investment logic. The majority of current robo-advisors aim to allocate their clients to managed ETF portfolios based on their preferences. It is expected that capabilities in the future will evolve into more advanced offerings such as automatic asset shifts and expanded coverage across alternative asset classes like real estate.

Robo-advisory can have a major impact on the personal finance and wealth management sectors. While current robo-advisor total assets under management (AUM) only represent $10 billion of the wealth management industry’s $4 trillion (less than 1% of all managed account assets), a Business Insider study estimates that this figure will rise to 10% by 2020. This equates to around $8 trillion AUM.

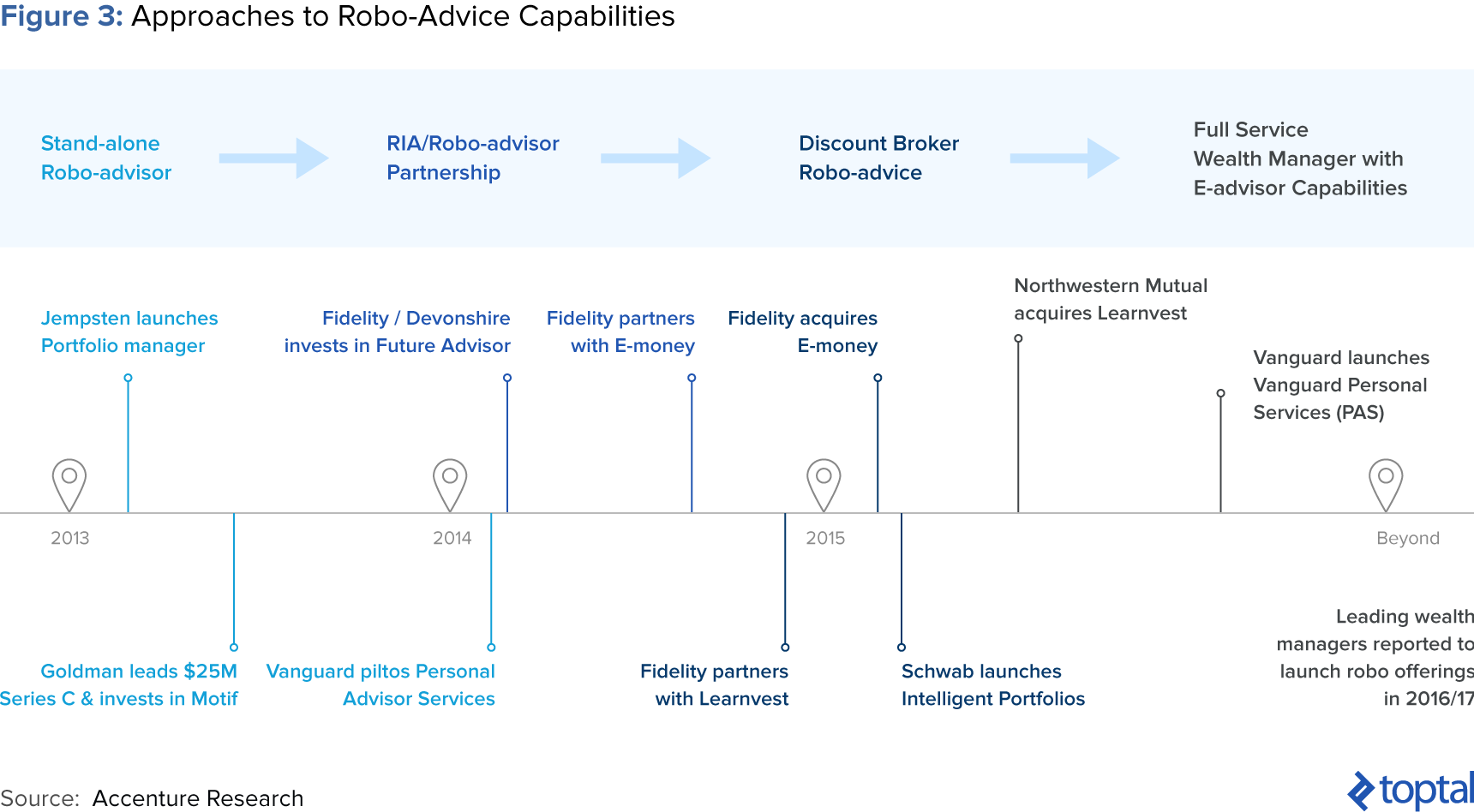

Industry Adoption of Robo-Advice

Industry players have adopted varied approaches to robo-advisory. Smaller wealth management firms are adding algorithmic components to automate their investment management, reduce costs/fees, and compete with robo-advisors. On the other hand, established investment firms are buying existing robo-advisors, such as Invesco’s acquisition of Jemstep or creating their own robo-advisor solutions, such as FidelityGo and Schwab’s Intelligent Advisory.

Robo-Advisors vs. Financial Advisors: Will Humans Be Replaced?

The general consensus among experts is that humans will remain indispensable. The human touch will remain critical, as advisors will still need to reassure customers during difficult financial times and persuade them with helpful solutions. A study performed by consulting firm Accenture revealed that 77% of wealth management clients trust their financial advisors while 81% indicate that face-to-face interaction is important. For clients with complex investment decisions, the hybrid advisory model, which couples computerized services with human advisors, is gaining traction.

While financial advisors will remain central, robo-advisors may cause shifts in their job responsibilities. With AI managing repetitive tasks, investment managers might take on the responsibilities of a data scientist or engineer, such as maintaining the system. Humans may also focus more on client relationship-building and explaining the decisions the machine has made.

Artificial Intelligence in Finance: Insurance Underwriting and Claims

Insurance relies on the balance of risk amongst pools of people; insurers group similar people together, and some people will require payouts while others won’t. The industry is built around risk assessment; insurance companies are no strangers to data analysis. However, AI can expand the amount of data analyzed as well as the ways it can be utilized, resulting in more accurate pricing and other operational efficiencies.

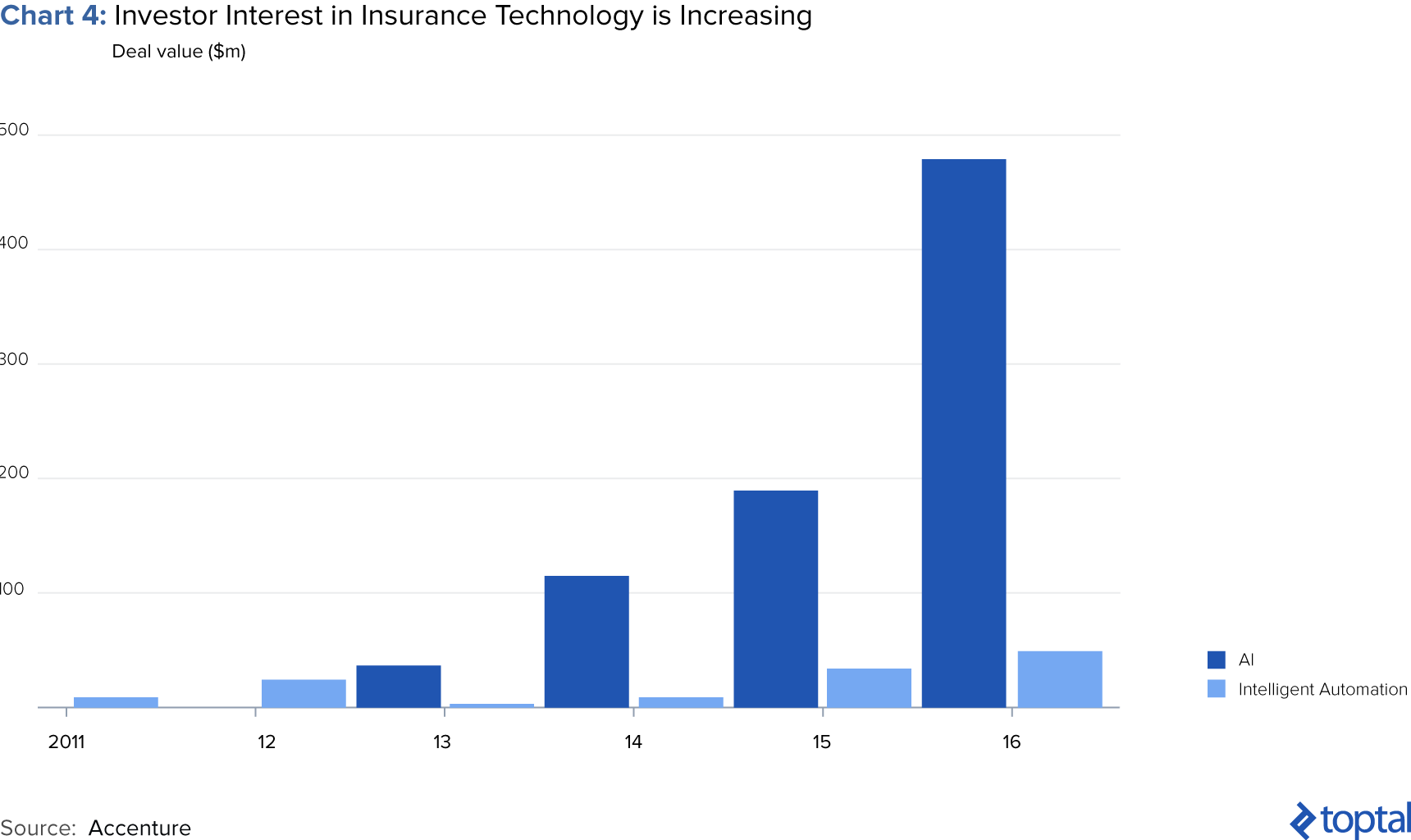

Startups are at the forefront of pushing the industry forward. According to Henrik Naujoks, a partner at Bain & Co, “The start-ups are showing what is possible and what can be done. A lot of incumbent executives are looking at it — they don’t really understand it but they want to get involved.” Investors have also caught onto this trend (see below). In 2016, AI was one of the most popular themes for insurance tech investment.

Artificial Intelligence and Underwriting

A PWC report predicts that AI will automate a considerable amount of underwriting by 2020, especially in mature markets where data is available. Currently, an insurance underwriter, with the help of computer software and actuarial models, evaluates the risk and exposures of potential clients, how much coverage they should receive, and how much they should be charged for it. In the short term, AI can help automate large volumes of underwriting in auto, home, commercial, life and group insurance. In the future, AI will enhance modeling, highlighting key considerations for human decision-makers that may otherwise have gone unnoticed. It’s also predicted that advanced AI will enable personalized underwriting by company or individual, taking into account unique behaviors and circumstances.

Enhanced underwriting may leverage not only machine learning for data mining, but also wearable technology and deep learning facial analyzers. For example, Lapetus, a startup, wants to utilize selfies to accurately predict life expectancy. In their proposed model, customers will email their self-portraits, which computers will then scan and analyze—analyzing thousands of regions of the face. The analysis would consider everything from basic demographics to how quickly the person will age, their body mass index, and whether they smoke. In addition, wearable technology could make the underwriting process more collaborative. Instead of relying on lengthy medical checks and complicated contract processes, wearables can provide real-time insights into policyholder health and behavior. Clearly, machine learning in finance is already evolving.

These types of nuanced, real-time risk analyses will enable not only more accurate customer pricing, but also early detection of health risks and an opportunity for insurance companies to invest in prevention. Instead of eventually paying for costly treatments for the patient, insurance companies can proactively try to lower the probability of damages and associated costs.

In a 2013 Oxford study analyzing over 700 professions to determine which were most susceptible to computerization, insurance underwriters were included in the top five most susceptible. Even where AI does not completely replace an underwriter, AI automation can alter an underwriter’s responsibilities. AI can free up an underwriter’s time for higher value-add, such as assessing and pricing risks in less data-rich emerging markets, providing more risk management and product development feedback.

Artificial Intelligence and Insurance Claims

Insurance claims are formal requests for payment sent to insurance companies. Insurance companies then review the claim for validity and pay out to the insured once approved. Here’s how artificial intelligence can enhance the process:

Improved customer data accuracy. The claims process is fairly manual: Human agents manually log customer information and incident details. According to an Experian report, data quality can suffer: incomplete data accounts for 55% of data errors, while typos comprise 32%. AI can improve accuracy by reducing manual input. In addition, claims processes often require insurance agents to match customer information with numerous databases. AI can be used to do this more efficiently.

Faster payout recommendations. According to a J.D. Power & Associates property claims satisfaction study, slow claims cycle times are one of the largest contributors to customer dissatisfaction. AI can help to reduce turnaround times by first validating the policy, then making determinations on the claims and whether to automate payment. This is because AI has the ability to analyze not only structured data, but also unstructured data like handwritten forms and certificates.

Artificial Intelligence in Finance: Conversational Banking and Customer Service

Banks are making big bets with their client-facing virtual assistants, known as chatbots. While the early versions of chatbots will only be able to answer basic questions about spending limits and recent transactions, future versions are slated to become full-service virtual assistants that can make payments and track budgets for consumers. Engaging with customers can translate into significant cost savings, but human interactions are also undoubtedly more complex than straightforward number crunching. Critics point to chatbots’ lacking of empathy and understanding, which humans might need when dealing with difficult financial decisions and situations. For this technology, AI technology of natural language processing will be essential for processing and responding to personalized customer concerns and wishes.

In October 2016, both Bank of America and MasterCard unveiled their chatbots, Erica and Kai, respectively. These will allow customers to ask questions about their accounts, initiate transactions and receive advice via Facebook Messenger of Amazon’s Echo tower.

Capital One has also launched their own chatbot, named “Eno,” which is an anagram for “One.” Eno enables customers to chat with the bank using text-based language to pay bills and retrieve account Information. Barclays is also getting in on the action. In describing Bank of America’s new chatbot, Michelle Moore, the head of digital banking at Bank of America declared, “What will banking be in two, three or four years? It’s going to be this.”

Parting Thoughts

The full impact of artificial intelligence in financial services is to be seen. Some futurists have argued that the world is rapidly approaching a tipping point, coined “singularity,” where machine intelligence will surpass human intelligence. Famous technologists and scientists, including Bill Gates and Stephen Hawking, have warned about this point. Elon Musk has also famously urged, “AI is a fundamental existential risk for human civilization, and I don’t think people fully appreciate that.”

As AI continues to proliferate our personal and professional lives, many issues will continue to emerge. These include the potential for mistakes, a general sentiment of distrust towards machines, and concerns about job replacement. It would be a mistake to disregard these fears. Still, society is already on an accelerating path forwards towards an AI-driven world. In this new world, it could be most productive to focus on how machines and humans can best co-exist. It will be important for policymakers to remain cautious, allowing new technologies to develop while monitoring and minimizing their negative consequences. Developers and designers should also enhance the ability of humans to understand AI systems to build trust and increase satisfaction with AI applications. Everybody will have a role to play.

As Haruhiko Kuroda, Governor of the Bank of Japan orated in a 2017 AI and Financial Services conference, “It is essential for us to constructively consider desirable ways in which humans and AI complement, rather than confront, each other. For instance, human judgment is not completely free from existing paradigms, and thus is sometimes negligent to changes. In this regard, AI could adjust our bias by neutrally analyzing and finding new correlations among a myriad of [sic] data. Meanwhile, humans could compensate for AI’s weakness with their intuition, common sense, and imagination.”

Understanding the basics

What is AI?

Artificial intelligence is defined as an area of computer science focused on creating intelligent machines that function like humans. AI computers are designed to perform human functions including learning, decision making, planning, and speech recognition.

What are the applications of AI in fintech?

AI offers opportunities for increased operational efficiencies in areas ranging from risk management and trading to underwriting and claims. While some applications are more relevant to specific sectors within financial services, others can be leveraged across the board.

What is a robo-advisor and how do they work?

Robo-advisors provide algorithm-driven financial services with minimal human supervision. Human financial managers have been utilizing automated portfolio allocation since the early 2000s but, today, robo-advisors allow customers direct access. Robo-advisors monitor the markets non-stop and are available 24/7.

What is considered fintech?

Fintech involves technology that enables banking or financial services. It can be used to describe anything from cryptocurrencies to robo-advisors for portfolio management.

What is an algorithmic trading system?

Algorithmic trading involves using computers programmed to follow a defined set of instructions for placing a trade. It leverages complex techniques like deep learning and machine learning. AI trading software can absorb enormous volumes of data to learn about the world and make predictions about the market.

What is a deep learning system?

Deep learning is a subset of machine learning. It’s facilitated object recognition in images, video labeling, activity recognition, and perception. Many draw the comparison between deep learning technology and biology, but experts agree that while inspired by the human brain, it’s not necessarily modeled after it.